The original Python notebook is on Github. Download it if you would like to follow along.

This IPython notebook solves the competitive storage model for the price of storable commodities using collocation as the numerical method. We reproduce an example from section 9.9.2 of Miranda and Fackler’s Applied Computational Economics and Finance using Python and independently of the authors’ CompEcon MATLAB toolbox.

The problem

The competitive storage model is a simple model for the price of a storable commodity. It has an uneven empirical record but it provides a good illustration of the computational problems which arise in modern macroecnomics.

We consider a commodity, say wheat, which can be stored subject to the condition that a fraction λ of the total stock at the end of a period disappears before the beginning of the next period and a cost per unit cost c has to be paid for storage. In each period there is an addition to stocks due to a stochastic harvest z and a reduction in stock from an outside demand given by a demand function P(q).

Storage decisions are taken by competitive speculators who must form expectations about future prices. These future prices depend on both the stochastic harvest in the next period as well as the total stock carried forward by all speculators taken together. We assume that speculators have rational expectations.The speculators are assumed to be risk neutral and discount their future profits by a discount factor δ.

Let st be the stock at the beginning of period t and xt be the stock at the end of period t and pt be the price that prevails in period t. Then the equilibrium conditions are, first that outside consumers should demand the quantity (st−xt) that is not stored,

pt = P(st−xt)

that the stocks in consecutive periods be linked according to the storage technology, st + 1 = (1−λ)xt + zt + 1

and most importantly the speculators maximize profits. pt ≥ δ(1−λ)[Etpt + 1] − c, with equality if xt > 0

The last equation has the complementary slackness form it has becuase speculators may be at a corner solution where they do not carry forward any stocks at all. If this is the case then current prices can rise above the expected future return from carrying stocks. On the other hand current prices can never be lower than expected future revenues in equilibrium since such a condition would produce an infinite demand for wheat by speculators in the current period.

The solution algorithm

It is known that the above system of equations has a solution of the form pt = ϕ(st). However there is generally no analytical solution and the function ϕ(⋅) must be computed numerically.

Suppose we expect that prices next period are governed by the function f(st + 1). Then the price function this period, say g(st), will be a function of this expectation through our equilibrium conditions above. We express this relationship in the form

g = Tf

where T is an abstract operator representing the working of the equilibrium conditions. It is precisely the property of a stationary rational equations solution that it is a fixed-point of this operator

ϕ = Tϕ

i.e., the expected law of prices is such as to produce behaviour which confirms the expect law of prices.

In order to find an approximate solution to this fixed-point equation we restrict our search to the finite dimensional space of Chebyshev polynomials of a given degree. The true solution may not lie in this space and thus no function in this space may satisfy the fixed-point equation at all points. In order to nonetheless get a good approximation to the true solution the collocation method we use in this notebook requires that the function come close to satising the fixed-point equation at a given finite set of points. In this notebook we take these points to be Chebyshev nodes. The task of finding the Chebyshev polynomial which satisfies this condition is carried out through successive approximation: starting from an initial guess f0 we calculate yn = (Tf0)(xn) at our chosen Chebyshev nodes xn. Then f1 is then taken to be a Chebyshev polynomial that passes through the points (xn,yn). This is continued until we reach a fixed point.

There are two more technical difficulties. The operator T involves computing a conditional expectation in order to find expected profits. For arbitrary functions this cannot be done exactly and we have to make a numerical approximation. In this notebook we use Gauss-Hermite quadrature to replace the continuous distribution of the shocks zt by a discrete approximation.

Finally, we need to work with a bounded state space for our calculations. If λ > 0 and z̄ the maximum possible realization of the shock then the beginning-of-period stock can never exceed z̄/λ. This however does not work when λ = 0. Also using this bound is harmful even when λ > 0 since this forces us to consider very large values of stock which are not reached in equilibrium, thereby wasting computational resources. We therefore follow the literature in arbitrarily assuming that there is an upper abound xmax on end-of-period stocks. The value of this parameter is adjusted to be large enought that it is never reached in equilibrium.

See Judd, Numerical Methods in Economics, Chapter 11 and 17 for more details as well as alternative algorithms. Section 17.4 discusses the competitive storage model.

Imports

import sys

import math as m

import numpy as np

from numpy import linalg

import scipy.optimize as spopt

from numpy.polynomial.chebyshev import Chebyshev

from numpy.polynomial.hermite import hermgauss

from scipy.stats import rv_discrete

import scipy.io as spio

import matplotlib.pyplot as plt

from collections import namedtuple

%matplotlib inlineCollocation

Collocation in general

def collocation_solve(T,fhat,nodes,fit,

log=True,tol=1e-6,maxiter=500):

"""

Try to solve the operator equation Tf = f.

We use successive approximations to find a function fhat in some function

space such that Tfhat = fhat at all points in `nodes`.

Inputs:

T(fhat,s): return (Tfhat)(s)

fhat: initial guess for fhat

nodes: collocation nodes

fit: a function when called as fit(x,y) with x and y

as arrays, returns an element phi of the chosen

function space such that phi(x[i]) = y[i]

log: if True prints progress messages

tol: tolerance parameter for stopping criteria

maxiter: maximum number of successive approximation

iterations to try

Returns:

Either `fhat` if success or `None` if iteration count exceeded.

"""

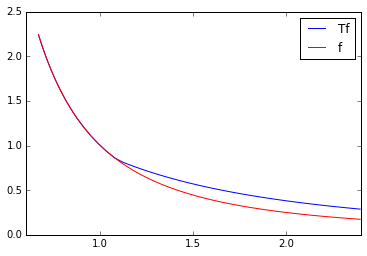

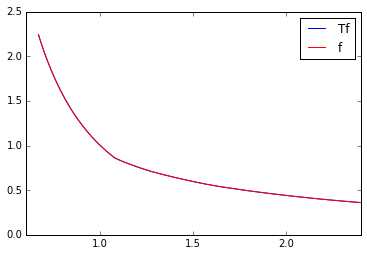

for i in range(maxiter):

lhs = np.empty_like(nodes)

rhs = np.empty_like(nodes)

for j,s in enumerate(nodes):

lhs[j] = T(fhat,s)

rhs[j] = fhat(s)

err = linalg.norm(lhs-rhs,np.inf)

if log and i%10==0:

print("Iteration {}: Error = {:.2g}".format(i+1,err),

file=sys.stderr)

plt.plot(nodes,lhs,"b-",label="Tf")

plt.plot(nodes,rhs,"r-",label="f")

plt.legend()

plt.show()

fhat = fit(nodes,lhs)

if err<tol:

return fhat

if log:

print("collocation_solve: iteration count exceeded",

file=sys.stderr)

return NoneCollocation using Chebyshev polynomials and nodes

def chebyshev_solve(T,guesser,degree,domain,

log=True,tol=1e-6,maxiter=500):

"""

Try to solve the operator equation Tf = f using

Chebychev collocation.

Inputs:

T(fhat,s): return (Tfhat)(s)

guesser: a function, `guesser(x)` gives a guess

for the function at point `x`.

degree: the degree of the Chebyshev series to use

domain: a list `[lower,upper]` of the domain over

which the function is to be approximated

log: if True prints progress messages

tol: tolerance to be used in stopping criteria

maxiter: maximum number of iterations for successive

approximation.

Returns:

Either `fhat` if success or `None` if iteration count

exceeded.

"""

nodes = Chebyshev.basis(degree+1,domain).roots()

def fitter(x,y):

return Chebyshev.fit(x,y,degree,domain)

f0 = fitter(nodes,

np.array([guesser(n) for n in nodes]))

return collocation_solve(T,f0,nodes,fitter,log,tol,maxiter)The competitive storage model

The problem data structure

# A competitive storage problem

StorageProb = namedtuple("StorageProb",

["cost" # Marginal cost per-unit stored

,"shrink" # Fraction of goods lost per period ($\lambda$)

,"yvol" # Log of harvest is distributed N(0,yvol)

,"xmax" # Maximum end-of-period stock

,"disc" # Time discount rate ($\delta$)

,"P" # External demand function P(q)

])Solution

# Solving the problem

class StorageSolution(object):

"""

A solution to the competitve storage model.

Constructor:

StorageSolution(prob,hgdeg=5,cdeg=50,

tol=1e-6,maxiter=500,log=True)

hgdeg: degree of Gauss-Hermite

discretization of shocks

cdeg: dgree of Chebychev polynomial to use

tol: tolerance for stopping criteria

maxiter: maximum no of iterations

log: if True print progress report

The model is solved in the process of constructing

the object, so constructor calls are expensive.

If the model cannot be solved in the give number of

iterations throws a ValueError. Computational

problems can cause an AssertionError to be thrown.

Instance variables:

Saved from constructor: prob, hgdeg, cdeg, tol

Others:

smax Maximum beginning-of-period stock

smin Minimum beginning-of-period stock

zs An array of discretized harvest shock values

ws An array of probability weights

corresponding to `ws`

phi The computed price as a function of

begining-of-period shocks

storage_revenue(phi,x)

Discounted expected revenue net of storage

costs per unit stored when the pricing

function is `phi` and end-of-period stocks

in the current period is `x`.

opti_storage(phi,s)

The optimal amount to store when the pricing

function is `phi` and beginning-of-period

stocks is `s`. Rational expectations is

built in: the expected stocks tomorrow is

consistent with storage decision taken.

T(phi) We want T(phi,s) = phi(s) for all s.

"""

def __init__(self,p,ghdeg=5,cdeg=50,

tol=1e-6,maxiter=500,log=True):

# Store input parameters

self.prob = p

self.ghdeg = ghdeg

self.cdeg = cdeg

self.tol = tol

# Compute Gauss-Hermition integration nodes

ys,self.ws = hermgauss(ghdeg)

self.ws = self.ws/m.sqrt(m.pi)

self.zs = np.exp(ys*p.yvol)

zmin,zmax = np.min(self.zs), np.max(self.zs)

# Bounds for beginning-of-period stocks

# Note xmax is maximum end-of-period shocks

self.smin = zmin

self.smax = zmax + (1 - p.shrink)*p.xmax

# Storage revenue computation

def storage_revenue(phi,x):

Etom = sum(

phi(z + (1 - p.shrink)*x)*w

for (z,w) in zip(self.zs,self.ws)

)

return p.disc*(1 - p.shrink)*Etom - p.cost

self.storage_revenue = storage_revenue

# Optimal storage decision

def opti_storage(phi,s):

P = p.P

xmax = p.xmax

if s>xmax and storage_revenue(phi,xmax) > P(s-xmax):

return xmax

elif storage_revenue(phi,0) < P(s-0):

return 0

else:

max_feas = min(xmax,s)

x_star,r = \

spopt.brentq(lambda x:\

storage_revenue(phi,x)-P(s-x),

0,max_feas,

full_output=True,

xtol=1e-5)

assert r.converged

return x_star

self.opti_storage = opti_storage

# Initial guess for pricing function

def init(s):

return p.P(s)

# We want T(phi) = phi

def T(phi,s):

x_star = opti_storage(phi,s)

ans = p.P(s-x_star)

assert ans>=0

return ans

self.T = T

self.phi = chebyshev_solve(T,init,cdeg,

[self.smin,self.smax],

log,tol,maxiter)

if self.phi is None:

raise ValueError("Failed to converge")

Visualization and simulation

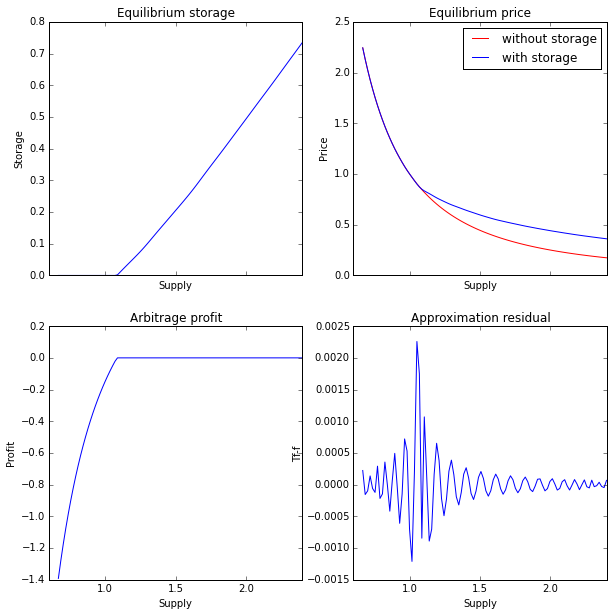

def illustrate(soln):

"""

Plot solution variables and diagnostics

``soln` is an instance of `StorageSolution`

"""

f,((ax1,ax2),(ax3,ax4)) = plt.subplots(2,2,sharex=True)

f.set_size_inches(10,10)

ss = np.linspace(soln.smin,soln.smax,100)

store = [soln.opti_storage(soln.phi,s) for s in ss]

ax1.plot(ss,store)

ax1.set_title("Equilibrium storage")

ax1.set_xlabel("Supply")

ax1.set_ylabel("Storage")

P = [soln.prob.P(s) for s in ss]

phi = [soln.phi(s) for s in ss]

ax2.plot(ss,P,"r-",label="without storage")

ax2.plot(ss,phi,"b-",label="with storage")

ax2.legend()

ax2.set_title("Equilibrium price")

ax2.set_xlabel("Supply")

ax2.set_ylabel("Price")

def optimal_profit(s):

x = soln.opti_storage(soln.phi,s)

return soln.storage_revenue(soln.phi,x)-soln.prob.P(s-x)

profits = [optimal_profit(s) for s in ss]

ax3.plot(ss,profits)

ax3.set_title("Arbitrage profit")

ax3.set_ylabel("Profit")

ax3.set_xlabel("Supply")

resid = [soln.T(soln.phi,s)-soln.phi(s) for s in ss]

ax4.plot(ss,resid)

ax4.set_title("Approximation residual")

ax4.set_ylabel("Tf-f")

ax4.set_xlabel("Supply")

def simulate(soln,niter,burnin=1000,s0=None):

"""

Run a simulation.

soln: An instance of `Storage Solution`

niter: The number of iteration for which to return results

burnin: The number of initial iterations to discard

s0: Initial beginning-of-period stock.

None selects the middle point of the domain.

Returns: arrays x and P of end-of-period stocks and prices

"""

xs = np.empty(niter)

Ps = np.empty(niter)

if s0 is None:

s = (soln.smin+soln.smax)/2

elif s0 > soln.smax:

s = soln.smax

elif s0 < soln.smin:

s = soln.smin

else:

s = s0

dist=rv_discrete(values=(range(len(soln.ws)),soln.ws))

phi = soln.phi

opti_storage = soln.opti_storage

shrink = soln.prob.shrink

zs = soln.zs

P = soln.prob.P

for i in range(niter+burnin):

x = opti_storage(phi,s)

z = zs[dist.rvs(size=1)]

if i>burnin:

xs[i-burnin] = x

Ps[i-burnin] = P(s-x)

s = (1-shrink)*x+z

return xs,PsExample from Miranda & Fackler

def isoelastic_demand(gamma):

return lambda q: q**(-gamma)

# Example from section 9.9.2 of Miranda & Fackler

mirfac_p = StorageProb(cost = 0.1,

shrink = 0,

P = isoelastic_demand(2.0),

yvol = 0.2,

xmax = 0.9,

disc = 0.9)

mirfac_s = StorageSolution(mirfac_p,tol=1e-10)Iteration 1: Error = 0.14

Iteration 11: Error = 1.6e-08

illustrate(mirfac_s)

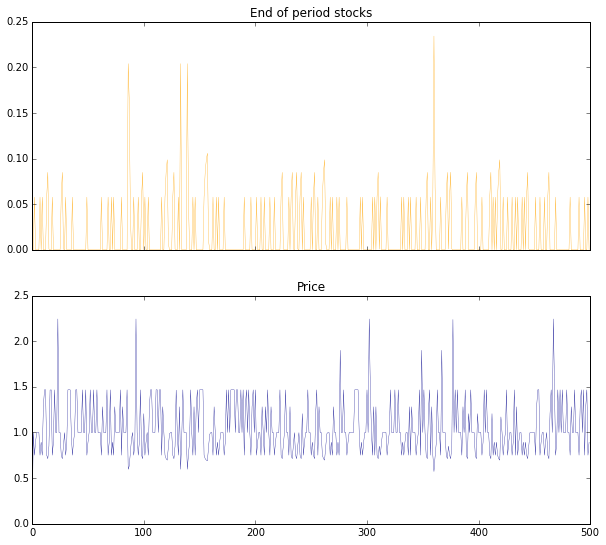

sim_N = 500

sim_xs,sim_Ps = simulate(mirfac_s,sim_N)

sim_so = (1-float(np.count_nonzero(sim_xs))

/sim_N))

print("Proportion of stockouts = {}".format(sim_so)

f,(ax1,ax2) = plt.subplots(2,1,sharex=True)

f.set_size_inches(10,9)

ax1.plot(sim_xs,linewidth=0.3,color="orange")

ax1.set_title("End of period stocks")

ax2.plot(sim_Ps,linewidth=0.3,color="darkblue")

ax2.set_title("Price")Proportion of stockouts = 0.71

<matplotlib.text.Text at 0x7f475ed685c0>